What I've Been Reading

Two weeks of news and filings.

5/31 - 6/13

Research Dump - News/Filings

Optimum is up almost 100% since announcing their restructuring about a couple weeks ago (link)

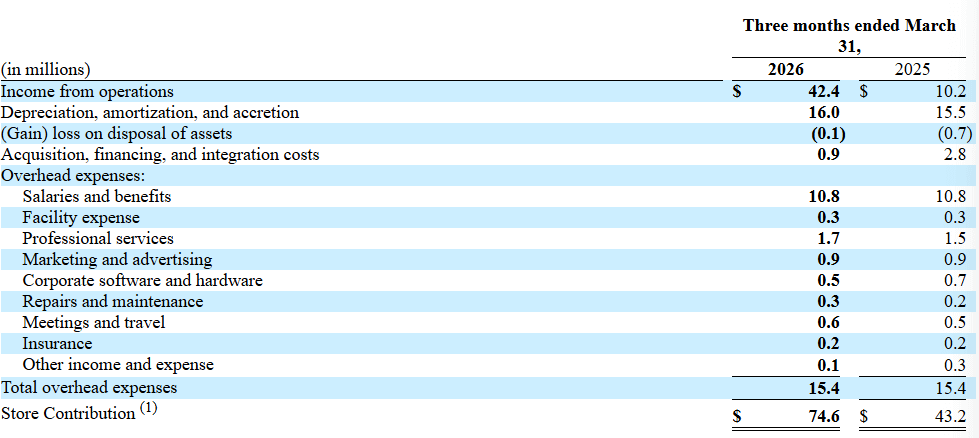

YSWY reported its first quarter as a public company

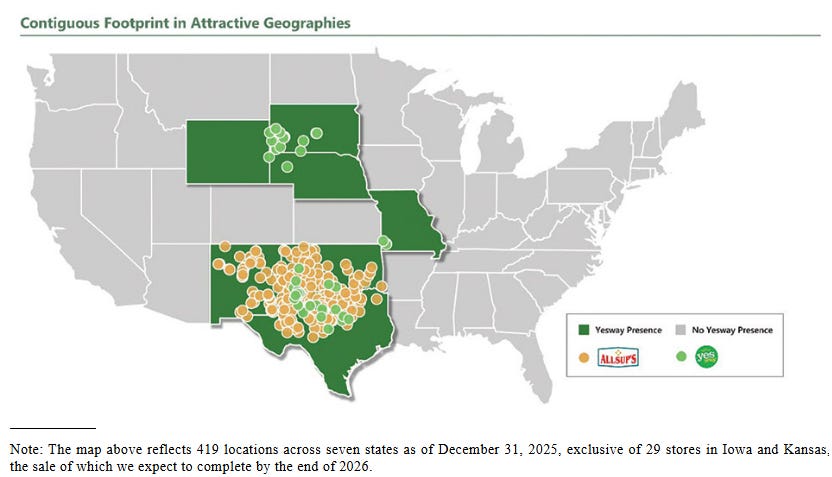

Based in Fort Worth

Inside merch SSS +4.5%

12 of last 13 quarters have been positive

Total inside merch +9.5% with a margin of 36.1%

SS Fuel Gallons +0.2%

Total +8.0%

Total fuel margin of 49.4 cpg (up from 35.9)

Total inside merch and fuel GP up 21.8% yoy

Fuel +38.5%

Merch +9.8%

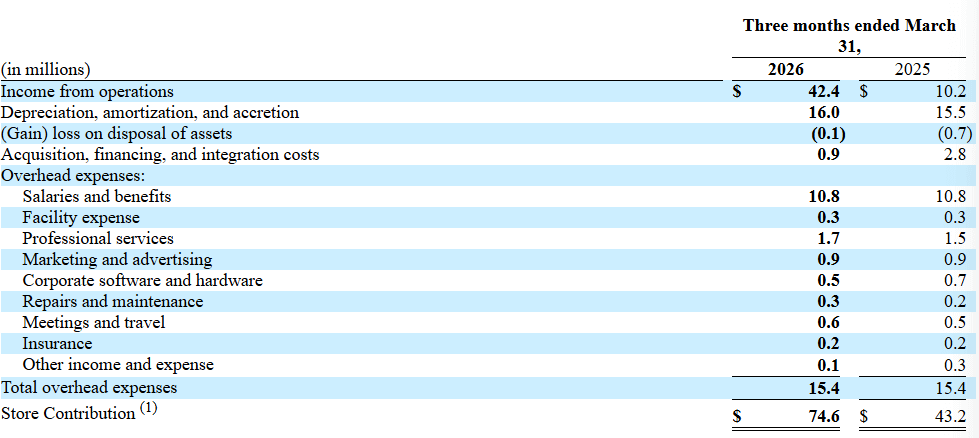

AEBITDA of $59m up from $29m last year

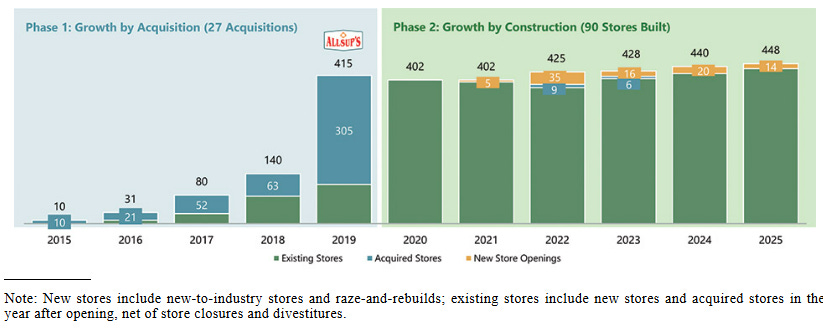

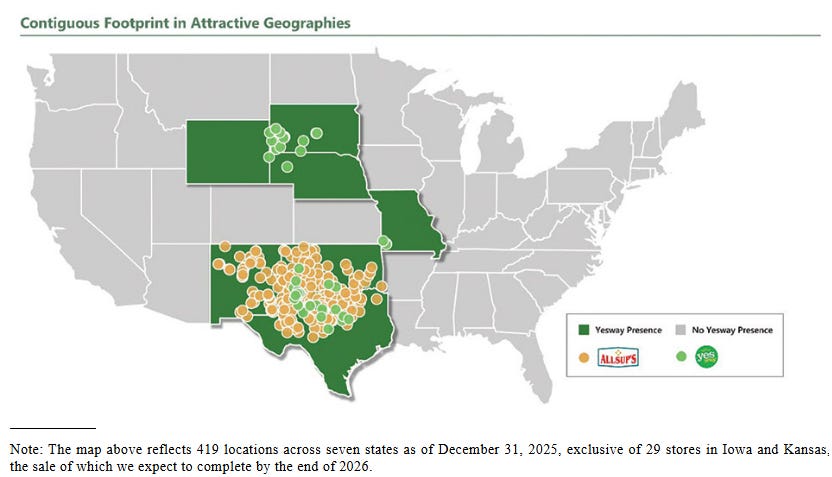

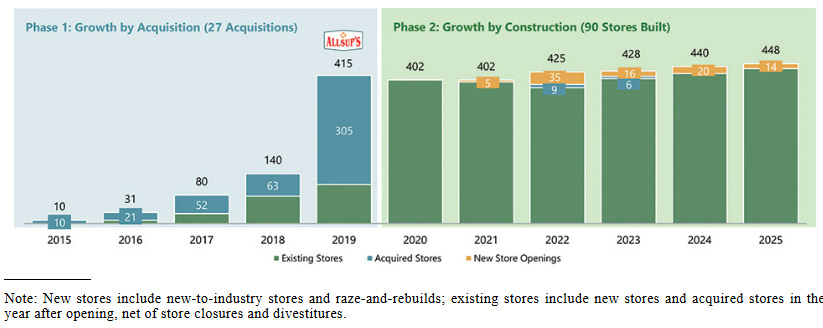

Currently operating 449 stores under Yesway and Allsup’s brands

$650m of financing and finance lease obligations vs $57m cash

~2.75x 2026E AEBITDA

~3.17x 2025 AEBITDA

~3.97x 2024 AEBITA

2026 outlook

SS Inside merch sales: +1.25-3.25%

AEBITDA $210-220m

Up from $187m in 2025, $149m in 2024… flattish 2022-2024 at $140-150m.

Capex $85-95m

Granular cost breakdown

“Results for the periods include 29 stores in Iowa and Kansas, which the Company expects to sell by the end of 2026… Store Contribution generated by the 29 stores in Iowa and Kansas was $0.2 million and $1 million in the three months ended March 31, 2026, and 2025, respectively.”

“Established in 2015 by Brookwood, a leading real estate-focused private equity firm, Yesway was built from the ground up by a team of seasoned industry veterans who brought decades of expertise and best practices to the convenience retailing industry.”

“Inside merchandise sales, which comprised 40.1% of total U.S. convenience retail industry sales in 2024, have increased by 6.1% per year on average since 1980, reaching $335.5 billion in 2024.”

“retail demand for fuel remains fairly inelastic with regard to fuel prices, with gas stations at convenience stores supplying an estimated 80% of retail motor fuel needs across the country according to NACS”

15th largest operator

“We operate predominantly under a company-owned, company-operated (“COCO”) model and own approximately 65% of the real estate underlying our total store base as of December 31, 2025”

DG reported 1Q results. FY26 guide:

Unchanged

Sales growth of 3.7-4.2%

SSS growth of 2.2-2.7%

Capex of $1.4-1.5b

Raised diluted EPS to $7.20-7.45 from $7.10-7.35 (50bps decrease on tax rate estimate)

~16x earnings

EXPE’s Ariane Gorin at Evercore

Uber deal: “So when Uber decided that they wanted to add hotels to their app, they, like any company, went out and talk to a number of players. And we won the deal. I believe we won because we have a strong value proposition on our supply, on our technology, on our servicing and it’s really it’s the full value proposition. And years ago, we would have all these internal debates about, well, is B2B incremental or not. And I just keep on going back to the size of the overall market.”

AI risk: “It is clear that people are starting more of their searches in AI search, whether it’s in Gemini and ChatGPT and Claud, wherever that might be. Now that traffic is still quite small. It’s less than about 1.5%. It’s growing fast, but it’s still quite small. And we’re doing a ton of work to make sure that our brands show up well there. And I think it’s an incremental demand source for us. So we’re doing work in AEO and organic. We’re doing work in paid. We’re early with ChatGPT on their paid ads. And I think to the extent that the top of the funnel is fragmenting a bit more, whether it’s with ChatGPT and Claude or TikTok moving into travel advertising more meaningfully, that is an opportunity for us. And the fact that we’ve been doing work over the last year in our marketing and be able to shift our marketing spend across channels based on a really good understanding of incrementality is really good timing for us. And then when you think about Agentic, we have opened our apps for agents to be able to come in because I want to experiment on everything. And again, it’s a very small part of even that 1.5% that I was talking about. And it’s early days, but from what we can see, what the agents are doing is they’re coming in and doing a bunch of discovery, but not going to the transaction. So again, I hesitate to draw too many conclusions from a small set of data. But I think what you’re seeing is agents going in, probably checking prices, trying to get a bunch of information, but that people aren’t yet comfortable allowing agents to actually make the transaction decision for them. Because remember, travel tends to be higher ticket value, higher order value. There are a lot of different decisions to make at the time that you make the booking. If it’s a hotel, what is the room type, what is the rate plan? Is it refundable? Is it nonrefundable? There are so many different things that you don’t necessarily want to delegate that to an agent.”

Natural language search: “Then there are the things that are more visible. So the conversation agents. We just rolled out natural language search on Vrbo. And so if you go to the Vrbo homepage, I think it’s about 50% of traffic right now, you can toggle and search by saying, you know what, I want to go to Tahoe, the last week of July with 8 people, I want a hot tub. We’re automatically going to pre-fill the dates, the destination. And then when you get to the search results page, the content is going to be personalized based on your search as well the results and the amenities and the filters and the like. What we’re discovering through that is we get more than 60% more information about a traveler in that kind of search than we did before, if someone just put in the destination. And so when you get that additional information, you’re able to personalize even more.”

OpenAI, Gemini, etc. as lead-gen partners vs booking agents: “Look, booking and servicing is complicated. There is catalog, there is making sure that you have constantly updated and accurate rates and availability. If someone tries to book something and it’s not the price they expected or the booking doesn’t go through, it’s a problem. You have to be there to solve it for them. If something goes wrong, afterwards, you need to be able to answer the phone or fix something in product so that people can make changes to their reservations. So I would think it’s an easier problem to solve around advertising and lead generation and a great travel experience and then leave kind of the tough work of the booking and the like to us.”

In my experience - OAI and Claude customer service has been pretty bad

ATNI completes initial closing of tower assets: “With net proceeds from the initial closing broadly the size of our annual Adjusted EBITDA, we are enhancing our liquidity and financial flexibility. This positions us to execute disciplined capital allocation and invest in opportunities that drive performance and deliver long-term stockholder value… the Company’s previously disclosed 2026 full-year Adjusted EBITDA1 outlook of $190 to $200 million is now expected to be $183 million to $193 million.”

APO selling 5m shares of HGV in public secondary. HGV to repurchase up to 750k.

SGI 30-day regulatory period for LEG has passed without challenge

Ron Duncan buying ~$1m of GCI stock (link)

“JPMorgan could be interested in Carlyle’s (CG) private credit unit, Carlyle Global Credit, should it ever be put up for sale, according to the report.”

UBS on SNBR closures benefitting SGI, per MT Newswire

“We think (Somnigroup) could capture meaningful market share over the next few years,” UBS analysts wrote, penciling in about 100 to 300 store closures by Sleep Number.

“About 200 closures could generate $120 million in sales for Mattress Firm parent Somnigroup, increasing earnings per share by $0.15, according to the brokerage. Those incremental figures rise to $200 million and $0.25, respectively, assuming 300 closures… More than 95% of Sleep Number stores were situated within five miles of Mattress Firm’s locations at the start of the year, UBS analysts said… Somnigroup’s premium brands have a “high degree of overlap” with Sleep Number’s $6,000 revenue per mattress, according to the note… “We don’t take this (bankruptcy news) as a negative read for industry demand over Memorial Day,” UBS said. “Several retailers (at a recent furniture and bedding conference) indicated healthy bedding sales over the key holiday period. Several also noted that rainy weather over the long weekend in certain parts of the country was a positive traffic driver.”

“Eric Haynor, who currently serves as the Company’s Chief Operating Officer, provided notice to the Company of his resignation as Chief Operating Officer effective June 5, 2026.”

Gas stations trade-up on strong CASY report ($4.57b rev vs $4.3b estimate; $4.37 EPS vs $3.31 estimate; cpg of 46.9 up yoy from 37.6) plus ceasefire appearing to be tested around same time.

JPM initiates on Bel Fuse with Overweight and $370 PT

John Zito (Apollo) not concerned about token maxing: “I think token maxing and token talk is for -- it’s a lot of BS, honestly. Like, if you look at per unit of knowledge and cost per unit of knowledge, prices are collapsing. Prices are collapsing per unit of IQ, if you did it that way. And so you have to bifurcate different types of compute into inference compute, which is most of us, like my IQ is not high enough to be able to use what Mythos 2 will be powerful enough. We’re not smart enough. I mean there’s only a handful of people that are smart enough to use these cutting-edge frontier models that need 180 IQ, 24/7, like the problem to solve for that, that’s where you’re seeing the prices go up. Our IQs are so low that we’re actually using that IQ to do like check out the recipe for the french toast and we’re spending tons of money. And so like, okay, so we have to figure that out clearly. So that we can manage case.”

RH FY26 outlook

Rev growth of 4.5-8.0%

AEBITDA margin of 14.2% - 16.0%

FCF of $300-400m (~8x FCF)

Incl. -270bps impact from pre-opening and startup costs for int’l

CRMT seems to have gotten into some trouble. Summarily

Oct 2025 - took a term loan from distressed credit fund Silver Point to help finance its ABS facility (backed by held loans)

Needed to find a new warehouse to finance further loans, didn’t get it done. Shut many locations.

As collateral quality declined due to increasing loss rates (allowance now ~25-26%), went into default. Searching for rescue financing. Had until June 12, extended a week.

Other / Misc.

APO’s next HQ is going to be in Austin

US government banning Fable 5 + Mythos 5 for any foreign national has led to Claude shutting off these models for everyone. I didn’t use Fable much anyway given it was slated to switch to usage based pricing soon.

Strong benchmarking

Trata (YC W25)@trytrataFable 5 (@AnthropicAI) scores 22% and tops the Hedge-Bench leaderboard. Running Fable was roughly 2X more expensive than Opus 4.8 per trial. For an industry where accuracy is mission critical, human judgement isn't going away6:07 PM · Jun 11, 2026 · 2.82K Views1 Reply · 5 Reposts · 27 Likes

Trata (YC W25)@trytrataFable 5 (@AnthropicAI) scores 22% and tops the Hedge-Bench leaderboard. Running Fable was roughly 2X more expensive than Opus 4.8 per trial. For an industry where accuracy is mission critical, human judgement isn't going away6:07 PM · Jun 11, 2026 · 2.82K Views1 Reply · 5 Reposts · 27 LikesHow many people really needed Fable anyway?

Gappy (Giuseppe Paleologo)@__paleologoClearly, Fable is doing a lot of work, and unleashing a ton of agents. To review a short technical note, it released 31 agents, coded simulations to verify my results, did "adversarial reviews". Eventually, it only made the assumptions slightly more rigorous. It is all good. For3:57 AM · Jun 12, 2026 · 156K Views58 Replies · 55 Reposts · 1.05K Likes

Gappy (Giuseppe Paleologo)@__paleologoClearly, Fable is doing a lot of work, and unleashing a ton of agents. To review a short technical note, it released 31 agents, coded simulations to verify my results, did "adversarial reviews". Eventually, it only made the assumptions slightly more rigorous. It is all good. For3:57 AM · Jun 12, 2026 · 156K Views58 Replies · 55 Reposts · 1.05K Likes

Great profile on someone who used to work with Mr. Beast. “There's very few people who understand how to get attention online better than him".” (link)

Is DCF dead?

Chairlift Capital@ChairliftCapDCF's died post GFC Multiples (Any) at an all time high

Chairlift Capital@ChairliftCapDCF's died post GFC Multiples (Any) at an all time high 4:40 PM · Jun 4, 2026 · 17.1K Views9 Replies · 10 Reposts · 120 Likes

4:40 PM · Jun 4, 2026 · 17.1K Views9 Replies · 10 Reposts · 120 LikesTwo PSAs - reach out if:

You know someone in London/UK looking for an analyst role

You need help finding your next analyst

Disclosure: This isn’t investment advice. I/we may own positions in securities mentioned.