What I Read This Week

5/22 - 5/30

This could probably be a couple different posts (and eventually will be - Research Dump, Misc. Links, Token Maxing, Factors) but here we go.

Research Dump - News/Filings

Barclays initiates on AEM at overweight. Yahoo: “Analyst Richard Garchitorena pointed out that the company is a low-cost gold miner, with more than 85% of its production coming from Finland and Canada… track record of driving share returns with acquisitions, including O3, Yamana, and Kirkland Lake… planning three acquisitions in Finland… continues to work on growth opportunities within its current assets. Barclays expects growth to begin in 2028… currently trading below its historical 10-year average EV/EBITDA multiple of 9.2x… a Canadian gold mining company. With operations in Canada, Finland, Australia, and Mexico, the company is one of the world’s largest producers of gold.”

Barclays also initiated on Cameco (TSX: CCO, NYSE: CCJ) at equal weight (Uranium)

CPAY refi increased liquidity by over $1b and extends maturity to 2031

Saw in a Form 4 that Arie Kotler sold covered calls on his ARKO stake, kind of interesting. $9 strike but looks like it’s small portion of his overall holding.

CCOI selling 10 DCs for purchase price of $225m. Expected to close “on the later of June 12, 2026 and the expiration or termination of the applicable waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976” (30 days).

Dollar stores: “Dollar Tree may face a modest earnings reset as recent grocery price increases appear to be getting rolled back, while weak shopper response and softer store-level trends may weigh on results, Oppenheimer said in a note Tuesday.”

Also DB: “While it’s been a rough few months for shares of (Dollar General) and (Dollar Tree), we are incrementally more cautious not only on the low-end consumer ... but also these models’ ability to absorb/mitigate rising energy costs at a time consumers seek affordability,” Deutsche Bank analyst Krisztina Katai said.

PR: Dollar Tree now offers on-demand delivery from its full U.S. footprint of more than 9,000 stores through DoorDash”

DLTR +15% on earnings on 3.5% comp, AEBIT up 110bps, $595m repurchases ($23b market cap at time of writing), increased FY26 adj EPS outlook to $6.70-$7.10 (stock is at $116). That is up from $6.50-$6.90 and vs FactSet consensus of $6.67. FY revenue expected at $20.5-$20.7b (Street at $20.6b). 2QFY26 comp guided to 2.5-3.5%. Opened 113 new DLTR stores. CFRA: “We view the guidance raise positively, particularly against weakening consumer sentiment and likely freight headwinds from rising diesel prices. However, we remain skeptical on growth sustainability given persistent traffic declines and questions surrounding the multi-price rollout’s impact on the company’s value proposition and long-term growth algorithm.”

DLTR: “Q1 results reinforced confidence that improving traffic trends and margin gains could support further upside in the shares, Truist Securities said in a note on Thursday.”

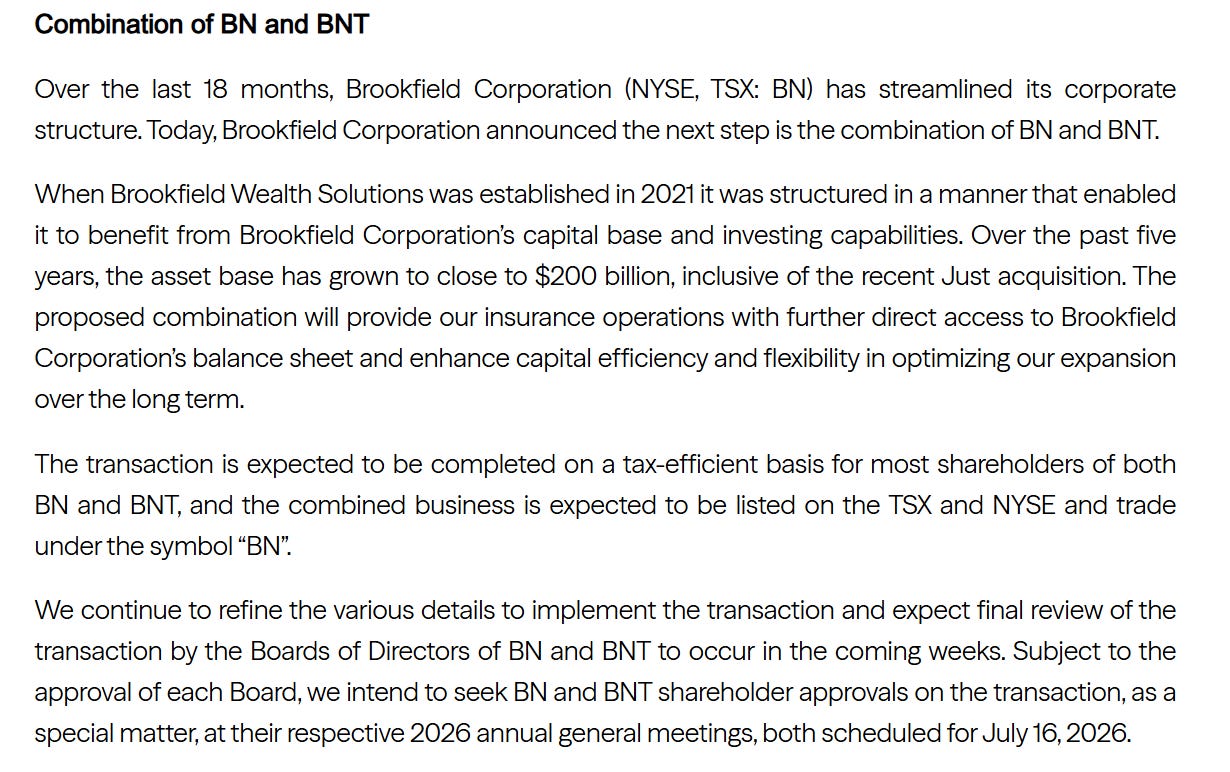

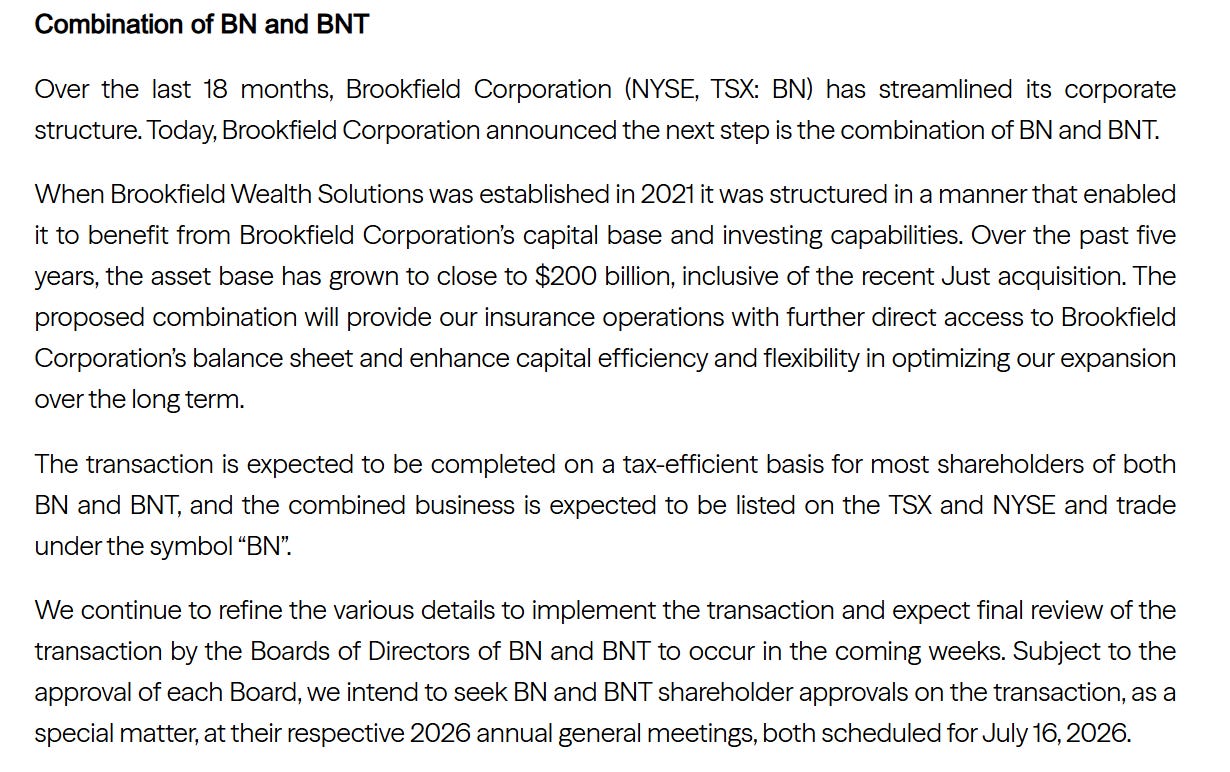

BN and BNT

Initially structured this way to raise capital for BWS without diluting BN shareholders. Not sure I fully understand this/why change now?

META testing AI chatbot subscriptions - one version $8 the other is $20. Rolling out in Singapore, Guatemala, and Bolivia.

BRZE: “We are off to a strong start in fiscal year 2027, delivering the fourth straight quarter of organic revenue acceleration, driven by strong demand for our AI-powered customer engagement platform,” said Bill Magnuson, cofounder and CEO of Braze. “The strong market momentum we experienced at the end of fiscal year 2026 carried directly into this quarter. Our AI solutions, including BrazeAI Operator™, BrazeAI Agent Console™, and BrazeAI Decisioning Studio™ are already delivering measurable results for customers.”

I don’t know much about Braze - anyone have a sense as to how much AI is really contributing here? Is this an AI winner? I know the team is very impressive in terms of pedigree, to the point it wouldn’t be super surprising had they figured this out and positioned themselves appropriately.

APO at Bernstein

President Jim Zelter on insurance headlines vs reality, disclosure, etc.: “you can either fight the conversation or engage in the conversation. And we probably try to do a bit of both, but first engage. So to your point, about 3 or 4 weeks ago, we put out on a Friday, what I would think is the seminal piece on the portfolio breakdown of the Athene book, all the sub-asset classes in granular detail. We put out a second piece on our alternatives book, the granular detail. And the third piece was all the affiliated or related parties… So the compendium of all 3 was a -- I don’t want to say a shot across the bow, but it was our attempt to say, listen, let’s -- if you want to shed light on it, let’s shed the light on the facts. And we’ve had a universal great response from regulators, from industry consultants and folks that are in the know on really what matters… Now in the world that we are in today, a lot of folks who cover these complicated businesses don’t have the historical benefit -- and I’m being very polite here -- to understand really how these businesses work. I think that if I could push back on one thing, I would push back on PE-controlled, the idea that Apollo happens to be an alternative manager. We happen to have a PE business. But the idea that the PE funds control our insurance activities, that couldn’t be further from the truth.”

Outlook on direct lending losses: “There’s lots of predictions from the big banks about where high yield and loan defaults will be over the next 3 to 5 years. And I’d use those as a starting point. And just because of the nature of direct lending and it was concentrated in software, I think you probably got to add a few hundred basis points of potential losses in direct lending to the high-yield and loan markets. Now I would say the high-yield and loan markets have been pretty benign the last several years, and there’s a massive CapEx cycle. So I think there was some estimates that -- I think one of the banks, UBS said 15%. That just seems extreme to me. So I suspect the disruption will cause a variety of defaults across all 3 product sets, high-yield, BSLs and direct lending. But I think if I had to guess if the 30-year average is around 3%, 3.5% default rates, the likelihood of the 5-year trend being higher than that long-term trend is probably in the cards. But I don’t have enough to say that it’s going to be dramatically higher than that right now.”

Rutledge nearly out of CHTR (Form 4)

APO, BX, Anthropic, GOOG, AVGO: “Apollo and Blackstone are working to bring in additional investors for about $36 billion in debt financing tied to Anthropic’s artificial intelligence infrastructure expansion, Bloomberg reported Thursday, citing people familiar with the matter. The report said the debt would be used to buy custom AI chips from Google, which Anthropic would then lease for its operations. Bloomberg reported Broadcom, which helps Google develop the chips, is backstopping payments on the largest portions of the transaction. The report said Apollo and Blackstone plan to sell down part of the debt while retaining significant portions themselves, with the deal expected to close next week.”

Misc. Links

Chris Hohn profile https://www.ft.com/content/521d1861-82c5-4194-9358-f3dd53d122b5

Harvey monthly token usage going exponential (link)

How is AI being monetized - Cost savings & op improvements, current rev monetization, and emerging AI benefits (link)

Social media has become less social

Good for META investors (me), bad for META users (also me)

New Street thinks Starlink subs could approach 100m by 2034 (link)

Dan Loeb on Invest Like the Best (link)

CS Lewis on creative ambitions

Dylan O'Sullivan@DylanoA4C. S. Lewis with maybe the most important paragraph ever written for people with creative ambitions

Dylan O'Sullivan@DylanoA4C. S. Lewis with maybe the most important paragraph ever written for people with creative ambitions 5:01 PM · May 28, 2026 · 402K Views36 Replies · 1.2K Reposts · 6.96K Likes

5:01 PM · May 28, 2026 · 402K Views36 Replies · 1.2K Reposts · 6.96K LikesSome companies are trying to adapt to the affordability crisis by offering e.g. smaller packaging, value deals, etc. Becoming more about volume and less about price (link)

Global equity markets are converging on the AI theme (link)

Rick Rubin on creating for your own taste (link)

SVP of Exxon on how we could get $150-160 oil (link)

Brad Gerstner on software multiples. Lots are just back to a market multiple now, and who knows whether that is even the right place. “If you get on the AI train, if you get in the token flow, you’re gonna get an above-market multiple. If you don’t, if you slow down and it looks like every time that computational intelligence improves, your business gets worse, then I promise you, [you] will trade below the market multiple.” (link)

Token Maxxing

This was the topic of the week and seems like one of the biggest risks to the AI trade right now. Basically - companies have been doing things like e.g. requiring or incentivizing employees to max out token usage and this has led to sprawling, ineffective use cases of AI. I believe this is a real problem at some companies. I also believe, in the near-term, it could derail the AI trade. But medium/long-term, I do not view this as an issue. It’s like telling the whole office they can order in and then being surprised when the DoorDash bill explodes.

Another interesting piece of this is the exponential nature of AI. On the one hand, this makes any possible drawdown in the AI trade likely to be short lived because it’s only a matter of time before the positive datapoints start to pile up again from the companies using this correctly. On the other hand, certain end-user demand (think people taking Ubers, for example) cannot possibly grow exponentially, and so token usage does need to be kept in check.

Cloud hyperscalers went through a similar period of customer spend optimization a few years ago.

Uber’s COO says it’s getting harder to justify the money spent on AI tokenmaxxing (link)

Corporate America Is Starting to Ration AI as Cost Skyrockets (link)

The best meme on this so far (link)

“the returns to expenditure on agents diminish much more quickly than the returns to expenditure on human labor” (link)

“The problem is that nobody understands token pricing. I literally have no clue what the cost of any of my AI use (coding or research) will be, or should be. All I know is that it is suddenly getting much more expensive, and I’m looking at local models I can run on my Mac.” … “I think you are right on both accounts. So the question is … if you are mgmt at a frontier lab looking to spend 100s of billions on compute. What gives you the confidence to do that?” (link)

An AI bear case from David Orr (link)

Due to the nature of the r/r as I perceive it above, I find it really difficult to figure out how to size the AI trade. It depends a lot on your goals and risk tolerance, which varies widely for readers and even I am still working out for my PA. If your goal is “beat SPY”, that’s a much tougher spot to be in than just compounding at an acceptable rate (10%, 15%, whatever it may be for you). And not even sure how to trade this environment if your goal is low vol. Prayers out to the tech pods.

Factors

Very new to this, so go easy on me, but I want to start writing about it more.

I recently started reading Giuseppe Paleologo’s Advanced Portfolio Management: A Quant’s Guide for Fundamental Investors (link). It has been a great reference for starting some basic PA analytics via Claude Code. A few notes:

First of all, I already knew Gappy was sharp from following him on Twitter. What I did not know was that he is also an excellent writer. Here is how the book opens. How do you not buy after reading this?

I wrote this book for equity fundamental analysts and portfolio managers, present and future. I am addressing the reader directly: I am talking to you, the investor who is deeply in the weeds of the industry and the companies you cover, investigating possible mispricings or unjustified divergences in valuation between two companies. You, the reader, are obsessed with your work and want to be better at it. If you are reading this, and think, that’s me!, rest assured: yes, it’s probably you. You were the undergraduate in Chemical Engineering from Toronto who went from a summer job at a liquor store to founding an $8B hedge fund. The deeply thoughtful Norwegian pension fund manager who kept extending our meeting asking questions. The successful energy portfolio manager who interviewed me for my first hedge fund job, and the new college graduate from a large state university in Pennsylvania taking a job as an associate in a financials team.

I imagine that these readers are at different stages in their careers. Since the companies they cover are fundamentally different, they do think in different ways. But they all share a feature: they all have valuable trading ideas but realize that having good ideas is useless without the knowledge of how to turn them into money. This is the objective of portfolio construction and risk management: how to put together a portfolio of holdings that will be profitable over time and will survive adversities.

Advanced Portfolio Management notes (cont.)

This book will teach you to:

Separate stock-specific returns from the investment environment

Size positions

Understand performance

Measure and decompose risk

Hedge risk you don’t want

Use diversification

Manage losses

Set leverage

As a Buffett acolyte (former? it’s complicated), the discussion of risk in section 3.4.1 hit hard for me. I’ve always defined risk as permanent impairment of capital. He wastes no time getting at the essence of this term - it is very difficult to define. Does it mean a holding going bankrupt? Investors redeeming? Large enough losses that you cannot meet funding obligations? The time horizon is also an important consideration. “In the long run we are all dead anyway.” It’s tough watching a fund pursue a strategy with a 5 year time horizon when the capital stack only gives you 12 months.

“Risk is associated to the probability of losses large enough to disrupt our ability to invest.”

Figuring out what disrupts your ability to invest is a hell of a lot easier said than done. How are you going to feel if your portfolio draws down 10%? 20%? How will your clients feel? Are you willing and able to live with the stress from a quality of life perspective? Will it impact the quality of your decision making?

For my PA, I’m still trying to figure out where I sit on the spectrum given my current life financial situation (may need the money at some point), goals (not sure about relative vs absolute yet), etc. I’ve also considered just trying to run a market neutral account to see what it’s like and better understand what I am up against. Though right now I figure trying to apply some of the factor analysis to my PA is a good enough place to start.

I’d be curious to hear from other L/O equity investors how they think about factor analysis, if at all. E.g. the previous discussion about sizing the AI trade is something all of us have to deal with. Do you just clone SPY exposure? Do you hedge it? How is this impacted by the incentives + structure you are investing within? What factors are you most exposed to and why? Do you manage to certain exposure levels or limits? What custom factors have you tested?

I am looking for the best publicly available quant data for looking at factors. This thread has turned up some good answers but if anyone has anything to add I am all ears.

Why momentum works (link)

A custom “factor” from Adam Parker - change in gross profit margin (link)

Other

I’ve been exploring the talent market for fundamental equity analysts. One subgroup I am looking to better understand and learn from is people transitioning (whether they are trying now, tried and failed, or tried and succeeded) from single managers (big L/O, Tiger Cub L/S, whatever) into the multimanagers. If this is a topic of interest for you please reach out, I’d love to ask some questions. You can DM me here, on Twitter (@stockthoughts81), or email me at stockthoughts81@gmail.com

Disclosure: None of this is investment advice and I/we may hold positions in securities mentioned.