Tidewater (TDW): a first-pass look

Largest pure-play owner of offshore support vessels

How the business works

Tidewater owns offshore support vessels (OSVs) and charters them to oil and gas operators. Revenue is close to one equation:

Day Rate × Utilization × # of Vessels

A vessel’s operating costs (mostly crew, repairs and maintenance, and insurance) are largely fixed once the boat is crewed and working, and fuel is generally the customer’s cost while a vessel is on-hire. So an extra dollar of day rate carries almost no extra cost and falls close to entirely to EBITDA. That operating leverage runs both ways: when utilization or day rates drop, the crew (generally) and insurance stay on the books, so margins fall faster than revenue. Tidewater went bankrupt at the 2017 trough when that ran in reverse, an oversupplied fleet meeting collapsing rates and a balance sheet with too much debt. Below EBITDA, depreciation and drydock amortization run about $260 million a year (the full step-down from adjusted EBITDA to operating income is a bit over $300 million once other items are included), which takes a roughly 44% EBITDA margin (FY2025: $598M on $1.35B of revenue) to a roughly 21% operating margin.

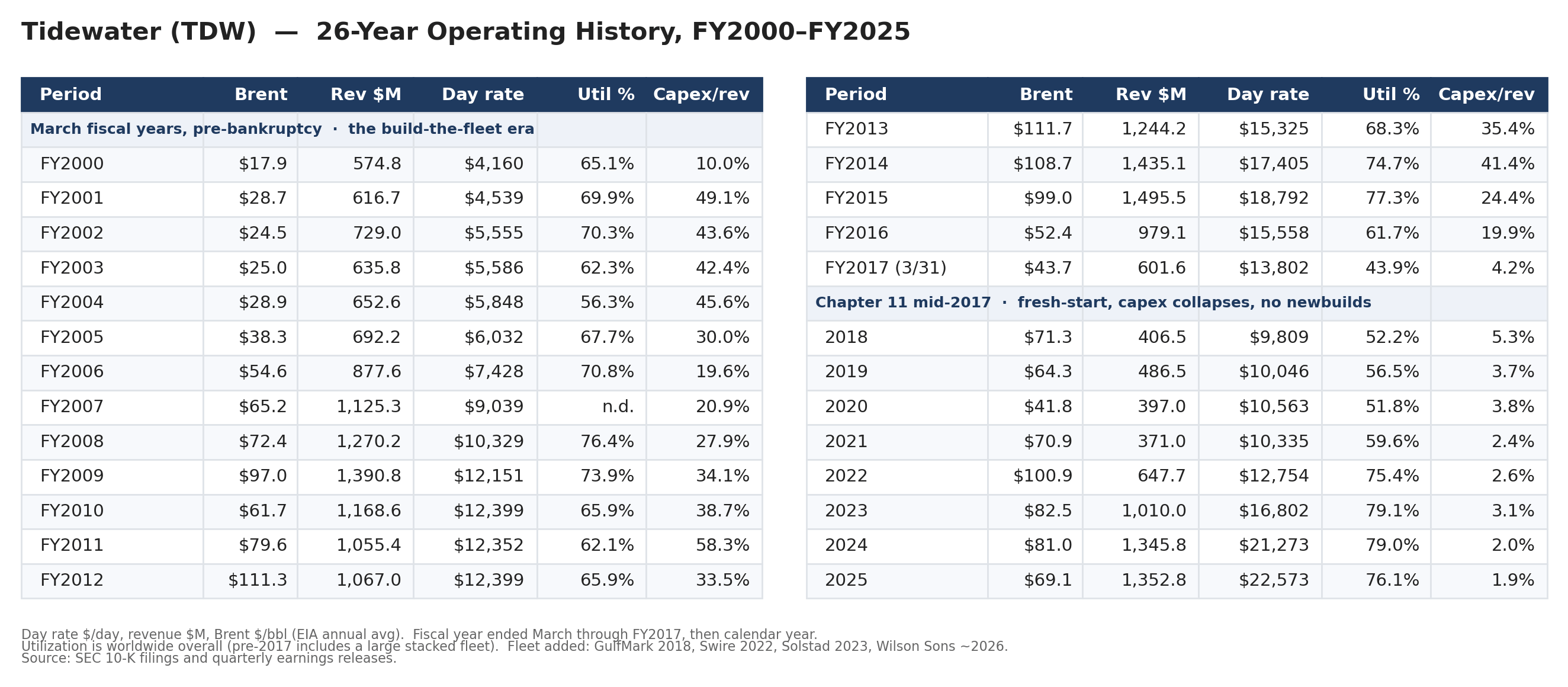

The 26-year cycle

Tidewater operating history, FY2000 to FY2025. Source: SEC 10-K filings; Brent = EIA annual average. Pre-2018 figures are March fiscal years (ending 3/31), each paired with the calendar-year Brent that overlaps most of it; calendar years from 2018.

Two things stand out in the history.

First, the current day-rate environment is strong even without $100 oil. Tidewater’s 2025 average day rate of about $22,600 is a nominal record. The prior peak, roughly $18,800 in fiscal 2015, was set after Brent had spent 2011 to 2013 above $100. Today’s rate environment has been reached with Brent closer to $70 to $80.

Second, capital intensity has changed dramatically. Before the 2017 bankruptcy, Tidewater routinely spent heavily on newbuilds, with capex reaching as much as 58% of revenue and typically running in the 25% to 45% range. Since bankruptcy, reported vessel additions have been closer to 2% to 5% of revenue, or roughly 9% to 13% if drydock maintenance is included. The company did not stop growing; it changed how it grows. Instead of ordering new vessels from shipyards, Tidewater has bought existing fleets (more on this in a second). Revenue across the full period has swung from $575 million to $1.5 billion, down to $371 million, and back to $1.35 billion.

The supply story

This is a key part of the thesis. Almost no meaningful new OSV supply is being built. Their investor deck has a lot of good data on this. Global shipyard capacity is down about 56% since 2008 (Clarksons), and the OSV orderbook sits near a record low. The existing fleet is aging out: the pool of under-25-year-old OSVs shrinks by roughly 48% over the next decade as vessels age past 25 (Spinergie). And the economics block new supply. Management estimates a newbuild needs a through-cycle day rate around $44,000 to earn its cost of capital, against a total-fleet rate near $22,500 today. On management’s math, day rates would need to nearly double before newbuild economics make sense.

Put another way, Tidewater’s enterprise value is about 40% of the roughly $9 billion it would cost to replace its fleet (VesselsValue, April 2026). On the latest call, management commented that they see the whole fleet repricing roughly $3,000 to $4,000 a day higher each year as legacy contracts roll onto current rates.

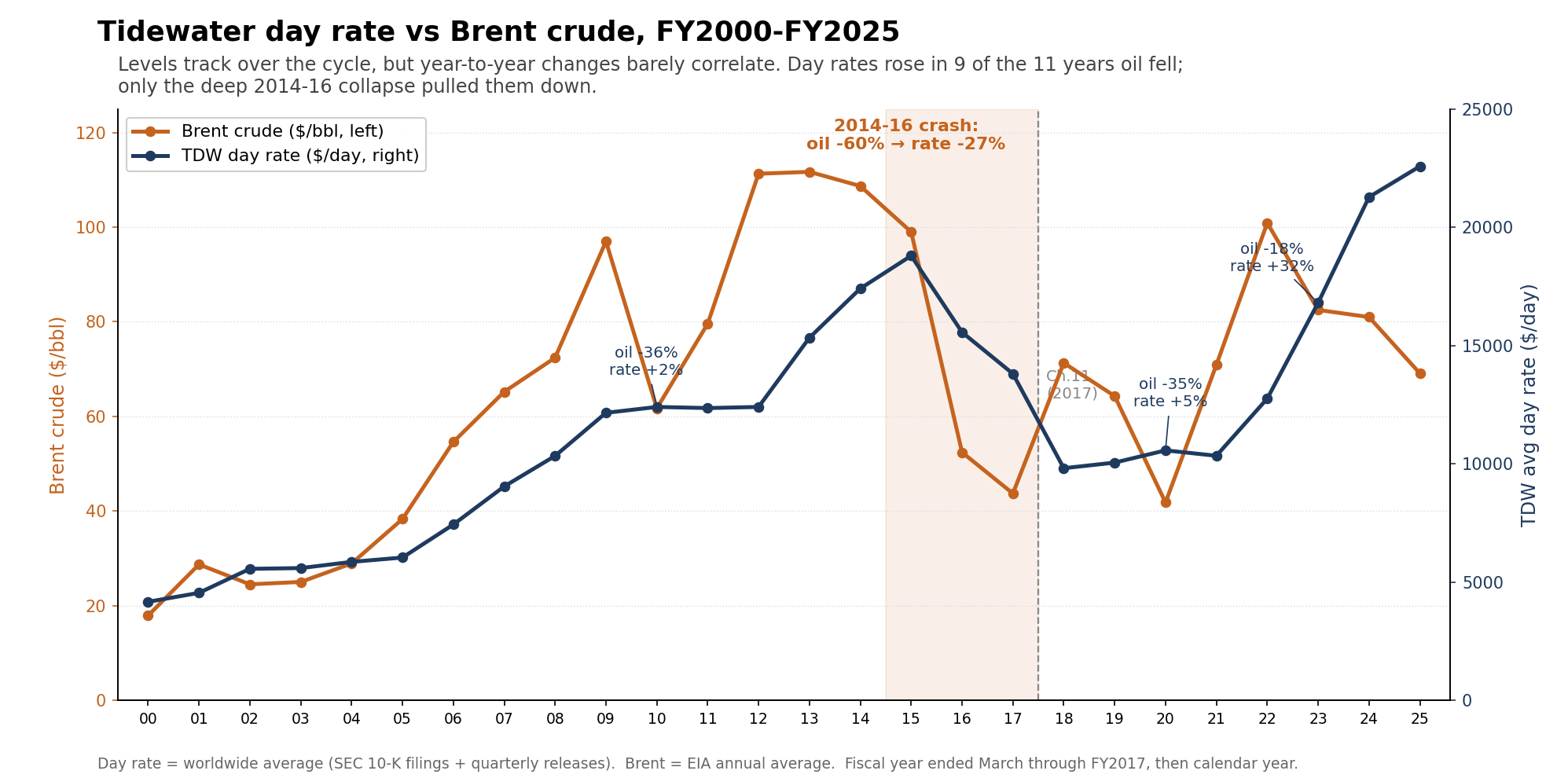

Oil is a risk, but not the driver

Worldwide average day rate vs Brent. Sources: SEC 10-K filings and quarterly releases; EIA. Pre-2018 day rates are March fiscal years; Brent is the calendar-year average.

Day rates and oil track over the cycle, but the year-to-year link is weak: day rates rose in 9 of the 11 years oil fell. The only time rates followed oil down was the 2014 to 2016 collapse, when Brent was cut roughly 60% over two to three years; even then rates halved with a two-to-three-year lag, from about $18,800 in 2015 to $9,800 in 2018, and the company went bankrupt. So oil is a real risk, but a high-bar one: it takes a deep, sustained collapse, not a normal pullback, and that last crash hit an oversupplied, actively-newbuilding industry that no longer exists. Contracts add to the stickiness: for the legacy Tidewater fleet, Q1 revenue plus firm backlog and customer options represented about $1.1 billion, or 84% of the 2026 guidance midpoint.

Management, the balance sheet, and the bear case

What draws me is how management uses capital. Tidewater has rebuilt itself by buying OSV fleets below replacement cost across the cycle: GulfMark in 2018, Swire Pacific Offshore in 2022, Solstad’s PSVs in 2023, and now Wilson Sons / Ultratug in Brazil - about $500 million for 22 vessels with roughly $440 million of below-market backlog, expected to close around mid-2026. This is also why the reported capex line looks so low: growth runs through deals, not the shipyard, and much of that growth has been funded outside the traditional capital-expenditure line. GulfMark was an all-stock merger, and most of the Swire consideration was paid in warrants. Net debt to EBITDA is just 0.2x today and should sit near 1x after the Wilson cash payment and assumed debt, still inside management’s limit. The core debt stack is long-dated, with a main 2030 maturity, though Wilson brings some rollover Brazilian debt. Management has also said it only wants to spend when it can return to net debt zero within roughly six quarters. Director Robert Robotti, a value investor, owns about 4.5% and was the most aggressive insider buyer near the lows; Seawolf also said on a recent episode of What Are We Doing that it added on the June drop.

Where I come out

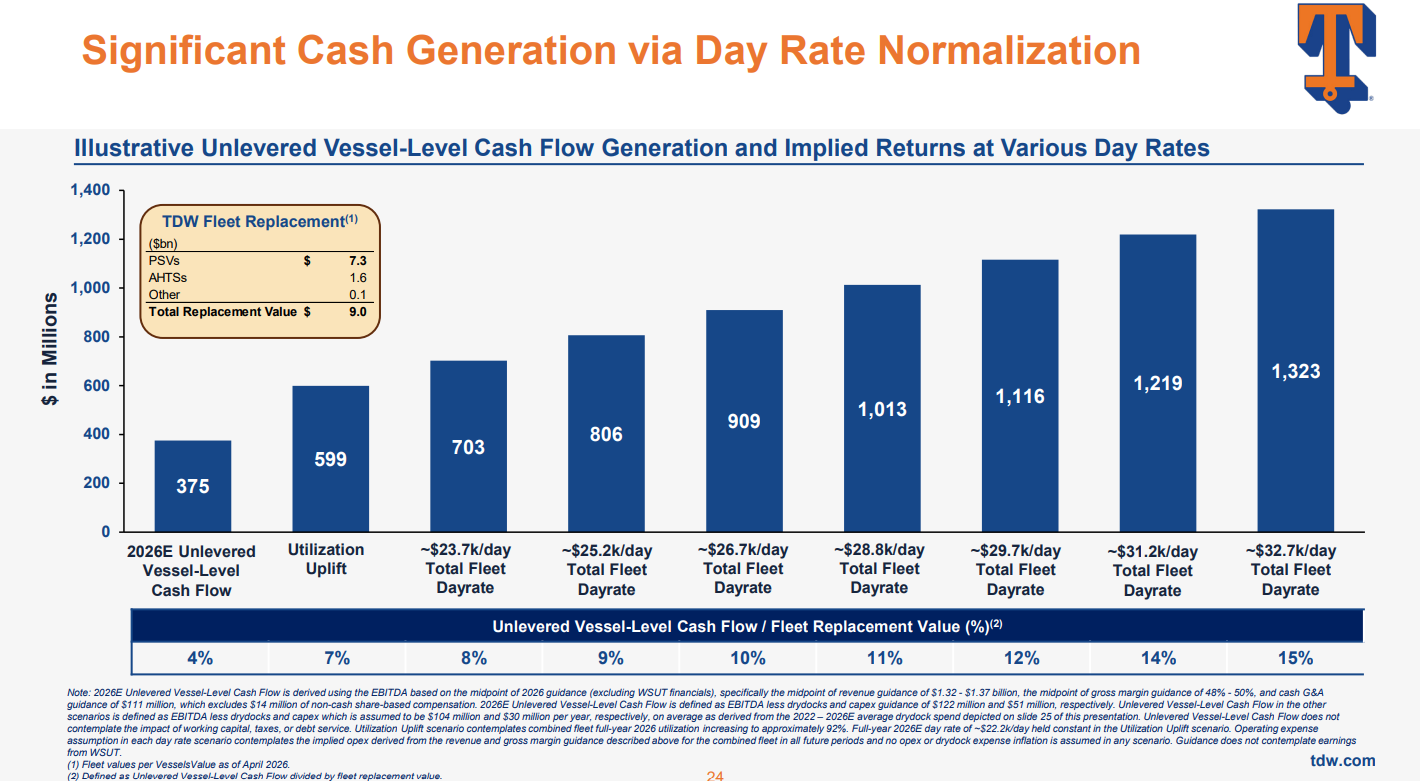

This is the kind of setup I find interesting at $66: a capital-disciplined operator that buys assets cheap, a clean balance sheet, and a supply backdrop that has re-rated day rates higher even on flat oil. The clearest way to size the upside is the gap to new supply. Enterprise value is around 40% of replacement cost, and the company’s own math takes vessel-level cash flow from about $375 million today toward $1.3 billion as the total-fleet day rate climbs into the low-$30,000s. Management estimates a newbuild needs roughly $44,000 a day to earn its cost of capital, so even that $1.3 billion case still sits below the rate that would justify building. In price terms, a ~1 turn rerating back toward historical averages plus modest growth is worth around +20%, a few thousand dollars a day higher on rates gets closer to +40%, and rates rolling back toward $20,000 is about -15%.

Credit: Tidewater May 2026 Investor Presentation.

What I’m still monitoring and thinking about

The downside threshold: last downturn, it took a sustained halving of oil to break rates. The supply side is tighter now which probably helps, but eventually demand gets hit.

Verify what percent of a customer’s offshore budget the OSV line is.

Wilson close and how management approaches capital allocation after it. Seems likely the buyback will resume soon enough, but it also sounds like there could be further M&A.

Disclosure: none of this is investment advice; I/we may own positions in securities mentioned.