Inside an Investment Analyst’s Mind: One Week of Daily Brain Dumps

Unfiltered thoughts on research, focus, and the pursuit of better investing

What I Worked On/Thought About This Week

I recently wrapped up an experiment: for one week, I spent 5–30 minutes each day writing a stream-of-consciousness “brain dump” about whatever I was working on or thinking about. I did a quick edit (or sometimes none at all) and posted those daily reflections to X (@stockthoughts81). Now that the week is over, I’m compiling them here in one place.

The goal was to clarify my own thinking, keep a record of my day-to-day process, and hopefully spark conversations with others tackling similar problems. These entries are closer to raw journaling than polished essays—maybe I’ll flesh them out more at some point, but for this first run, I kept it simple.

This is something new for me and I am considering continuing to do it and sending the full set via Substack at the end of each week. I’d love your feedback: is this of any interest to you?

If you enjoy this kind of journal-like content and want to keep following along, feel free to sign up below. And please don't hesitate to reach out with thoughts on any of the companies or topics discussed.

So for 1/19/25…

Today I didn’t do much work. I shouldn’t have done any work; it’s Sunday. But I thought about work a lot and did a little bit as well. The work I did was mostly pseudo-work. I updated my To Do List. I don’t know if I have the best system for this, but currently my “work mind” lives primarily in my email inbox as well as a Word document (To Do List). I pin and flag lots of emails. Some of these are e.g. ongoing discussions with vendors, other investors, events I might attend, etc. Others are news that needs to be reviewed at some point. I get a zillion emails a day from CIQ from all the companies I follow. Headlines, transcripts, and filings ranging from Form 4s to 10-Ks. And then the To Do List is the master list. Broken into a few categories: Big Three (try to maintain three big projects at a time), Admin, Time Sensitive/Deadlines, and When/If I Get Around To It.

The top project on my Big Three right now is ORCL. I’ve been working on it for a little bit. The other two are Aker BP and SNBR. My sub-tasks for ORCL are organized and ordered. First I need to cut down the Industry Description section of my report because it’s way too long and nobody wants to read all that. Then I need to do some preliminary valuation work because it’s gotten to the point I don’t want to spend too much more time if it isn’t cheap. Then fill out the barebones structure of Notes on my report. And finish by skimming gathered reading materials and adding to Notes as needed.

The Preliminary Valuation work has been a subject of some thought lately. I feel like I should do valuation relatively early on in the process so that I spend my time on ideas that have a high probability of being actionable. This seems commonsensical as far as making for an efficient research process. But sometimes I wonder if I end up relaxing my Quality standards (moat mgmt etc.) when I get the greed wheels spinning too soon. But I have a team to hold me accountable for that.

On Aker BP, I don’t have a clue what I am doing. I am still early there and have never looked at an oil and gas company. I think I would like to make a post on it soon so that people can tell me how wrong I am. I’d rather you tell me that, vs I go ahead thinking I am a genius and lose money. Anyway, so far, there is a ton that doesn’t make sense to me. But I’ll focus on one for now. It seems like sell-side analysts (or some of them anyway?) model it well-by-well. Something about this is confusing and/or intimidating to me. 1) I don’t want to do that, it sounds awful. 2) Shouldn’t the people who do that basically just always outperform? How much do results differ between analyst estimates when they do it this way? I guess it doesn’t consider future wells.

On everyone’s favorite heavily leveraged, vertically integrated mattress manufacturer, there isn’t a ton more work to do. There are a couple of calls I should probably do. I’d like to talk to creditors but I don’t even know if that is allowed or how that works. Would they talk to me? Do people do that as part of their research process? Even if I can’t talk to their creditors, I’d like to maybe talk to either a former creditor, or maybe their former treasurer or other finance execs, or some other creditor in the industry who knows how stuff works. All the credit agreements have signatures from each participating bank in the syndicate on it. If I can’t talk to currents, maybe I look at old ones. What I am trying to understand is the decision calculus from the creditors’ perspective. They already gave them some leeway bumping the covenants up. Why did they do that? Will they do it again? What is the process like if they were to go bankrupt? Wouldn’t it be a pain to take ownership of those assets? Don’t they think things will eventually turn?

Part of me thinks that when I start asking these kinds of questions, it is time to move onto something else. But part of me thinks this is a very compelling opportunity. SSB was like 8-9x net leverage in I think 2021 and then things kept getting worse. And competitively, they were in a totally different situation than SNBR was. Getting crushed by TPX, their head on competitor selling beds across the Mattress Firm aisle from them. SNBR creditors have already shown flexibility. They have a negative working capital model with getting paid up front when things grow. Barring a recession, I have a tough time seeing how this ends up in a ton of trouble. But I am not super familiar with how creditors make decisions which gives me some pause.

Well I have already been writing for over 20 minutes so I should wrap this up. The last thing I will note is I have been listening to Cal Newport’s podcast a lot and thinking about Deep Work. I am not doing good in this realm. I need to do better. This has been on my mind a ton so I am sure there is more to come on this.

Well that’s quite a bit and I don’t feel too inclined to edit. There you have it. Day 1. Have at it. Tear it to shreds.

1/20/25

$ORCL

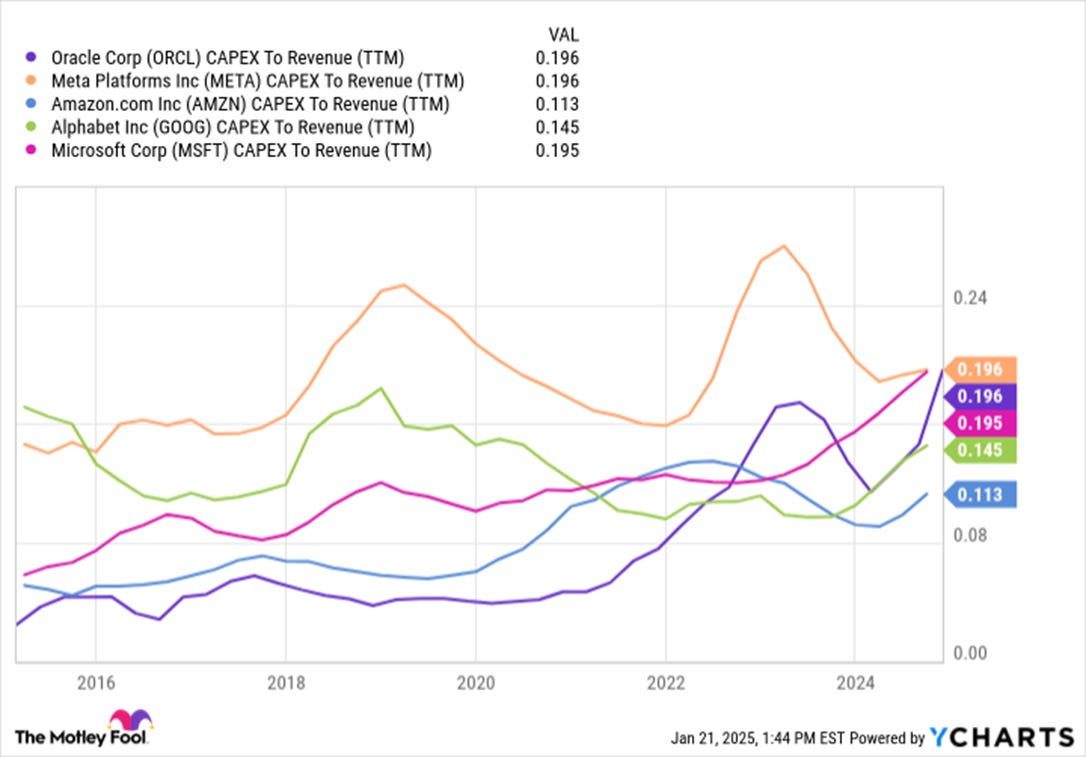

Day off today. Dabbled with ORCL. Cut down industry description and got started on preliminary valuation. Between the two of these things, I think I realize why there are so few concentrated positions in ORCL. It’s kind of a doozy. There are so many moving pieces. Sell-side diverges pretty significantly, especially on margins. Revenue growth everyone seems to be in the 10%-low double digit type range. But where does that come from? You have decently high margin SaaS revenue replacing really high margin on-premise support revenue. You have Cerner mix maybe shrinking back down somewhat. Maybe not, IDK. I don’t really even know what is the best way to break it down and think through it and model it. For this preliminary exercise it’s more of a reverse DCF type of exercise. But if I really want to own my thesis and numbers on it vs Street it almost certainly needs to be modeled on a level of granularity that the company doesn’t provide good disclosure for. Bernstein has done great work around this. From industry description perspective you have a lot going on. You have ERP exposure (defined broadly, including adjacent markets) maybe making up 35%ish of revenue between on-prem ERP, strategic back office SaaS, and database powering 3P ERP systems like SAP. ERP is most of the application biz. Then you’ve got a lot of the legacy business that was frankly kind of hard to get great data on. Bernstein estimates databases at like $17b revenue and cloud DB at like $2b run rate. Then you have OCI as the other big bucket and then a grab bag of services, hardware, non ERP apps, etc. OCI - they are gaining good share (apparently due to being low cost provider) but still really small vs big 3. Databases - IDK, this doesnt seem like a great setup. Most people are shifting away from using just one on-prem provider for this, and toward either using a cloud provider or a mix. Another tough thing on the valuation is free cash conversion. If you look at TTM capex/revenue for them and the hyperscalers, they are finally now just about leading the pack vs being much lower than the other for years. And going to double capex next year. Bernstein has (Capex-Depr)/(Adj Net Income) of -40-50% for them for FY25-27. This capex is about to become a huge drag.

Only other topic of discussion/thought today - gaining sell-side access at an emerging manager is HARD. Idk how to do this. There must be an approach that could eventually be boiled down to a script once you know what you are doing to try to get it for free for the first year. We have some but it’s tough. Need to just get more reps and try more. Can’t get what we don’t ask for.

1/21/25

More ORCL today. Some preliminary valuation work and filling out the report. Honestly, I am not seeing the vision on ORCL. I do not see the upside. I think a realistic range of cases is, on the low end: 6% growth for next 8y and then 4% in perpetuity, with 200bps margin decline from here and stay here. I get $82 PT that way. And then best case I see 14% for 8y and then 5% in perpetuity and margins up 700bps over 5y. I see $187 PT that way. Where is the upside scenario? Even just going very barebones. Let’s say I give them FY29 target of $104b. Maybe 45% “True” EBIT margin is $47b EBIT. Maybe $3b interest. 19% tax. $36b net income. 20x is $720b market cap. Over 4y is 10-11% compounding. And I mean, IDK, that kind of feels like giving them a lot and assuming everything works out in terms of favorable revenue/margin shift, cloud uplift more than offsets share loss in databases, etc. This is still all very back of the envelope at this point so I will need to check it closer later but I am just not seeing it. Maybe that multiple is too low. Maybe you say it should be 25x fwd instead. 25x47 = $1.18T over 3y. Now you get compounding in the 30s. I don't know, who am I to say what makes sense? It’s not super obvious to me. Street is already giving them $99b for FY29 so not that far off from target.

I was surprised to see how low the multiple has been historically. In the past couple years it had drifted well outside its historical range. In the past they always struggled to drive significant organic growth. In the 2000s it was always - these guys are going to have to buy their way to their growth targets. In the 2010s, you can see some lower reported numbers. It’s funny to look back to an Aug 2013 Morgan Stanley report. Basically says: “MSD rev growth, EBIT margin improvements, and repurchases can ‘potentially sustain’ LDD EPS growth… the 10x CY14 EPS valuation is ~40% below large cap software median P/E… base case assumes ‘Oracle sustains modest organic cc growth of L-MSD through CY14… fwd P/E returns to LT avg of 12x.”

The evolution of the capital allocation is interesting. NetSuite and Cerner only really notable acquisitions in past decade. Both seem reasonable enough to me. Not great, not terrible as far as I can tell. Paid a lot for NetSuite (did not know Larry owned 41% lol) but it pretty much panned out. Did a ton of repurchases at great prices but now stopped to pay down debt from Cerner deal. Will be interesting to see if they return to it afterward given price increase. And then there’s the capex. Now at 19% of revenue, in-line with other hyperscalers, and heading higher. This is a big drag on the valuation if you look at it on a FCF basis. Not sure how to think about that. I don’t really know/understand how the market views and values this capex. I don’t think it cares for the hyperscalers right now. It’s probably a bit less derisked on ORCL but I am not sure. But I feel like if you are giving ORCL 12% growth (my base case that gets me to $140), a lot of that has to be OCI. So you can’t give them the growth and then just ignore the fact that this capex is eating up a huge, huge portion of their FCF. Not sure how long that will persist for. But Bernstein has FY24-27 (Capex-Depr)/(Adj Net Income) of 40-50% ish.

I don’t know. Where am I wrong? Who’s to say if it’s 25x fwd P/E in 3y or 20x LTM in 4y? Lot of that depends on the narrative. I don’t really want to bet on the narrative here. Just too many moving pieces.

Was briefly on Patient Capital webinar today. Interesting $CVS pitch. They have a value of $90-105 on it. Stock is at $52. Turnaround situation. Under 9x this year's depressed earnings. 5% div yield. Earnings are depressed due to the MA biz at Aetna. Very poor underwriting. Whole industry had bad underwriting. High utilization, lower rate increase than expected. But it's fixable. Heard nothing but good things about new CEO (David). Expected to earn $5.10-$5.20 this year. Can get back up to $8-10 as they turn that biz around. Histoically traded at 10x. So, $90. High teens compounding and a 5% dividend.

Asked around a bit about the OTAs. My best guess is it’s the OAI agent thing. Which doesn’t concern me much. Same mitigating factors as GOOG disintermediation risk - no supply, no customer support.

Other than that, I had a lot of meetings. Four calls/meetings today. Hard to get into the deep work groove like that. Team meeting, couple vendor calls, and a call with a productivity coach from Done Daily. It’s from My Body Tutor. It is like Future Fitness (which I also recently started using) but for getting more stuff done. Kind of expensive but 30 day guarantee. We will see how it goes. Goal is to have someone hold me accountable for how I manage my schedule and what makes it into it. E.g. did I really need 4 calls today? Thinking of implementing a rule where I wait e.g. a week or something if I think of having a call or demo’ing some product. Sometimes after a week I’m like “whatever”. Batching admin, social media, etc. for rest of day.

1/22/25

$ORCL $UBER

Finished up the qualitative portion on ORCL today. The way we do things we first seek to answer the question - valuation aside, is the biz quality good enough to warrant a concentrated position in? I think the answer is “yes” and I will be surprised if the team disagrees. So more detailed valuation work likely to become, but I will also be surprised if that work changes my mind about what I posted yesterday. I just don’t think it is that favorably asymmetric. In addition to that, still some uncertainty on the margins. Your key reporting segment (cloud services and license support) had gross margins decline from ~95% in FY17 to ~76% in FY24. Cloud gross margins, I’d assume, are still fairly high so you’d think we are getting to the bottom of this soon. But who knows.

Usually listening to the most recent earnings call is the last thing I do in my process (on the first qualitative phase). Usually it isn’t that incremental (not much changes in a typical quarter and how useful is the call vs e.g. sell side or the IR deck). This time, I actually think it would’ve served me better earlier in my process. They share actually useful info on the call. And with some companies it seems like even the Q&A is from some kind of a script (I am looking at you, MTCH), but Q&A portion was solid here. There was some interesting stuff in there about OCI. It just sounds like they are killing it, frankly. The growth. The private cloud stuff is interesting. The late mover advantage. The derisked capex because they can scale up with demand. Making it easy to automate by making all the racks the same and all regions have the same offerings. But it’s tough to know how much to read into this mgmt team. Like when they say some of the best models in the world are trained on OCI because it is faster and cheaper, and that customers include OAI, xAI, NVDA, and Cohere, what exactly does that mean? What do those relationships look like? How much revenue now and in 5y? And then this “world’s largest and fastest supercomputer” thing - who knows?

I listened to the Fundamental Edge webinar on UBER and that was great. It is only available outside of Fundamental Edge for two weeks so take a look if you’re interested. If you own UBER maybe you will get a couple nuggets here or there. But if you are new it’s probably the best two hours you can spend. I am still not exactly sure what I think. I am new-ish. I hadn’t thought through this stuff much. It is a risk if 1-2 players dominate the AV market (e.g. especially TSLA). Whereas if you have some 3rd, 4th, 5th players, it’s more likely at least some will look to UBER for demand gen. There’s also just the simple idea of slowed growth even if this isn’t a business killer. Having a third player usually makes the 1 and 2 grow slower. Idk has the unit economics of AV will work out. Adds some operating expenses. All about utilization. There are just lots of different ways for things to play out. Not all of them seem so bad for UBER.

1/23/25

Did not get much done today. Thought briefly about some stocks. Games Workshop seems expensive. Rathbones core biz had inflows but IW&I still bleeding assets. Spent an hour or so on Clarity Markets. Seems really interesting - prediction market for KPIs etc. Honestly not much else of note to report on. Lot of admin stuff. Hopped on a Gartner webinar about AI agents but left after 35m. Call with a research vendor. Got Courtlink login so looked around on there a bit (still don’t really understand how transcript requests work). The OTA price action on the OAI Operator announcement was interesting. Caught up on some email etc. IDK. Something off about today. Having days like today is not good for anyone. Not me. Not the firm. I am kind of in between projects right now. ORCL pending qualitative approval. Didn’t want to deep dive Aker BP yet because didn’t have a ton of time to allocate to it today and there was some uncertainty in the schedule. But the difference in the quality of my day when I get at least a couple hours in of real, focused research vs when it’s just doing stuff that doesn’t matter as much is a lot. There was an exercise I spent a couple hours on today that consisted of ranking companies by quality. IDK. We kind of had to do it, I guess. Not sure. I got that done quicker than I expected so I guess that is good but it doesn’t feel like a high value activity to me.

The reflection is here and I think that is good because it’s concrete acknowledgement and thinking about the problem, but I don’t have a solution for this. And in some ways the problem itself is a little elusive to describe. Lots of these kinds of days seem to pop up. It is not fulfilling and it is not valuable. But IDK. More meetings tomorrow. Limited blocks of time available for extended focus time to be able to really get into stuff that matters. I’ll have to think about what i can squeeze in when i plan out the day later tonight. And figure out - what exactly is the next step on Aker BP and where in my day can I allocate the most/highest value uninterrupted time to that? It’s tougher when it isn’t the first thing in the day. Because once you start looking at emails and texts etc. the ability to focus is not the same. But it’s weird because I did quite well with that today. I had like 12 minutes of screen time on my phone almost 6 hours after waking up. We were going to have a two hour meeting in the afternoon and we ended up meeting for 15m and then rescheduling so that kind of threw things off a bit. Maybe I should have retimeblocked after that.

1/24/25

$BLK $RAT $GAW $BKNG $EXPE $ABNB $AKRBP $MKSI

Research meeting this morning. Took a couple hours. BLK is killing it. Interesting that 55-60% of all their assets are, in one form or another, associated with retirement, and NONE of those retirement assets are private assets. Big opportunity, and you hear all the PE players talking about it, too. RAT is doing alright. Anytime you have one wealth manager buy another you are going to have some clients leave. Usually happens within the first year. Seems like that is probably nearing its end. On top of this, the wealth managers need to focus on porting over the new clients and all the associated communications and paperwork. During that time, they are focused on maintaining vs building the book. Perhaps a good setup for a return to organic growth sometime in 2025. RAT seems cheap. And then we talked Games Workshop. Opinions vary widely. I don’t know, I am not crazy about it. I know it’s been around forever but how we do we know the future will look like the past? It’s a really interesting business but probably just not for me. Because - I think you need to be able to have the conviction to hold through volatility. If Games Workshop shrunk a bit for some reason and saw some sales declines, I would probably be inclined to panic sell. Not being immersed in the community, how can I have any idea what is going on? We decided on 126 GBP for midpoint fair value estimate vs 144 GBP current price. Then we ranked/reranked a list of 84 companies in order of quality. Why not, right?

Spent some time preparing for a prospective client meeting we have coming up. I am very curious to hear from other buyside professionals and allocators about how much time analysts spend preparing for and meeting with allocators, how much access allocators are given to analysts, whether analysts refer to their notes when talking about companies, etc. Lots of questions about just the different dynamics. The crux of my curiosity being - if you’re an allocator, wouldn’t you rather have analysts focusing on research vs knowing they are super available and prepped to talk to clients? The PM is understandable, that is a different story. My DMs are open or feel free to respond here.

Next, handled some admin stuff. MKSI repriced their debt again and did another $100m voluntary prepayment. Spent some time thinking about the AI Agent/OTA stuff. Bernstein put out a note. My initial impression is - well, I am not concerned about this yet. I have more specific retorts to the note and more thoughts on it but I don’t want to get too into it here. I want to do more reading and thinking and please reach out if you have thoughts about it.

I spent some time going through initial recasting of historical Aker BP financial statements. I don’t usually work on IFRS/international companies, nor oil and gas companies, so you can probably guess how this is going. It is going to be a slow process. I’ll have more developed thoughts later. My first thing is - this technical goodwill thing is kind of weird. It’s basically there just as an offset to a deferred tax liability that gets created because these Norwegian companies often have very accelerated depreciation schedules so the tax base of the assets is often much less than the fair value. All this technical goodwill will always be written down over the life of the assets, which is very finite for O&G. But then they also had e.g. an impairment in 2022 because the expected life of a well moved from 2032 to 2028. I think I will add back the technical goodwill impairments but I am not sure if I should add back the other stuff in my assessment of normalized earnings power (if normalized earnings power is even a relevant concept for O&G). It seems like that might be part of the game in O&G?

1/25/25

Didn’t really work today but still thought a lot about work? Idk, you know how these things go.

Random thoughts about China, DeepSeek, etc. Interesting how everyone things everything out of China is fake. I feel like some small allocation to China by US investment firms may be warranted? But what do I know. Trump and Xi seem to get along. Some days I think it’s legit, other days I think we are very obviously on a 10-20y path to conflict. Not sure how Taiwan plays out. I’m fairly ignorant on this stuff but I think everyone is, even the ones who talk about it. Who knows what is going on. Why does the US care so much about it? Because of their freedom? How much does the US government actually care about such things for other nations? Or are we somehow protecting our own strategic interests e.g. TSMC? When we get our own fabs does this whole thing just go away? Does Greenland, Mexico, Canada have anything to do with any of this? I am extremely ignorant on all this. If you can, invest with OLP and call it a day. If you can’t, I don’t know, maybe some 5-10% basket allocation makes sense. But then again - and I struggle with this a lot - is a basket approach even conducive to a concentrated strategy? I’ve thought about this with lots of stuff. E.g. an O&G basket. Or buying two players in a leading industry e.g. TW and MKTX. But it takes more time. I don’t know. Also - on DeepSeek - is it really bad for all the megacap tech capex? Or does it just mean AI is going to move along multiples faster than we thought when megacap tech incorporates DeepSeek methodologies (if it scales).

Heard some interesting thoughts about how much time analysts should spend with prospective/current clients. No right answer here. There is a spectrum that ranges from “starving artist” to “asset gatherer” and I think you want to be somewhere in the middle. Still thinking more about that.

ORCL maybe buying TikTok? OK, I guess?

Did some cursory information gathering on a small company involved in the semiconductor industry. Seems interesting. Found little info. Which leads me to believe I should not name it, but if you think you know what I am talking about maybe DM me? Idk, I may talk about it at some point. Very early here.

I am not sure what to think about this exercise yet. I think I kind of like it. I want to write more. And I want to do it in public. For lots of reasons. So this is one way of doing that. I think I’ll keep doing it. I don’t know how it evolves. These posts are not getting many views or much engagement. I am not sure why. I have put more time and effort into these posts than any of my other posts. And I think they have been more vulnerable, interesting, and honest. I don’t know if no one cares, or it’s a bad format, or something else. Then I lift a chart of ski prices from LinkedIn and it goes viral because everyone says “yeah but season passes”, or some random podcast excerpt from a PE exec. I don’t think I really get the algo. I might play around with the format. E.g. maybe I ask Claude to convert all this into 280 character bits and schedule 8 tweets to go out in the next 24 hours. And then provide the long form via email or something once a week. IDK.

1/26/25

Items of note today: 1) I do not like IFRS. 2) Went to church. 3) Took a walk outside. 4) Decluttered.